$INTU is down 20% today, and half of finance Twitter posted the same take.

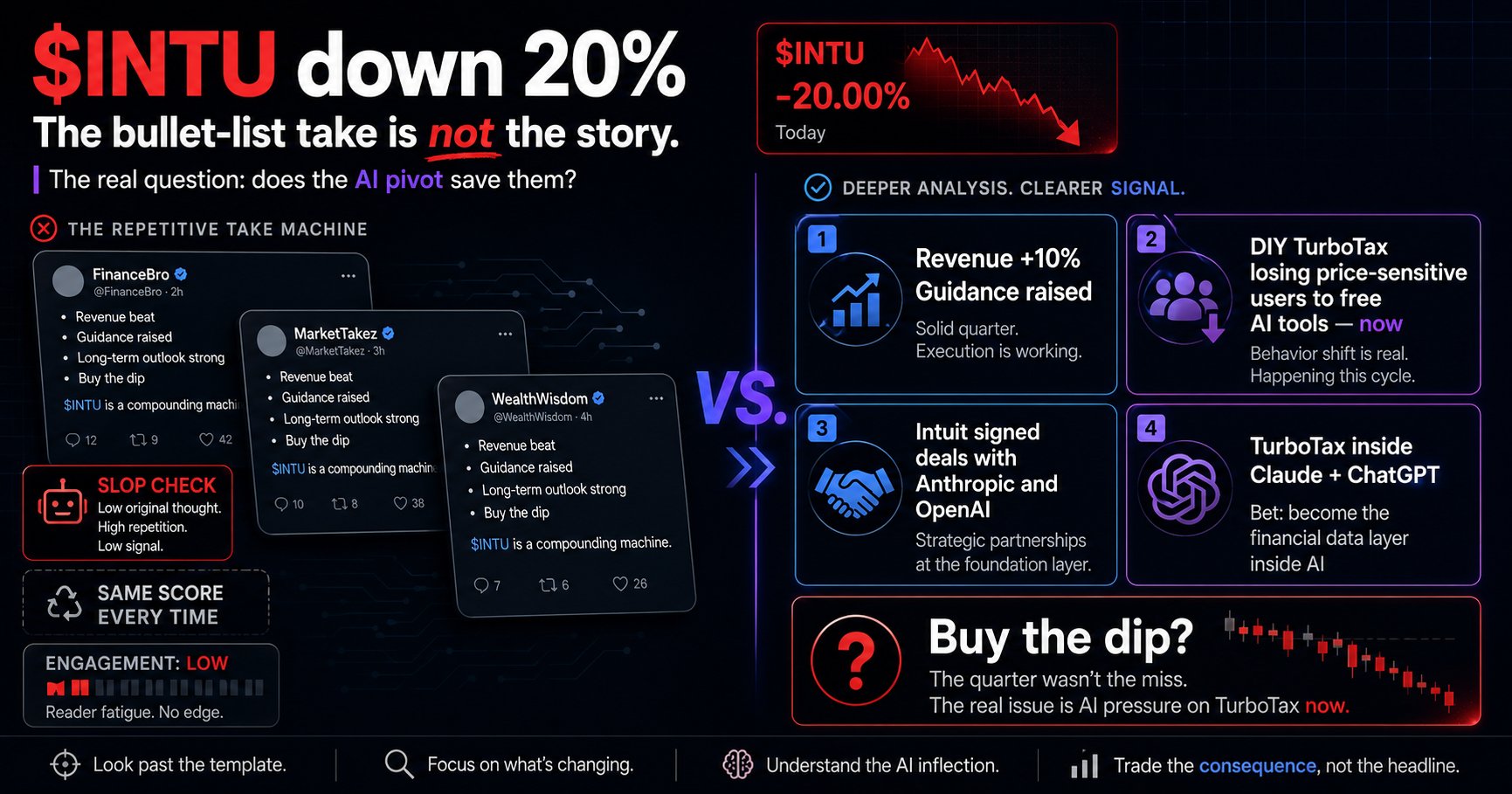

The earnings were technically solid. Revenue up 10% year-over-year to $2.67 billion, guidance raised for next quarter. EPS hit estimates. By the mechanical rules of earnings season, Intuit should have held or gained. Instead, the stock cratered 20% in a single session. Every finance Twitter account responded with the same template: bullet points, numbers versus estimates, closing question mark, zero actual conviction about what to own.

The algorithm clocks that structure in two seconds and kills the reach. But that's not the real miss. The real miss is that Intuit is losing the DIY tax segment right now, not in 2026, and the market finally priced it in. According to Intuit's own SEC filing language and earnings call, the TurboTax user base in the self-directed segment contracted this quarter. They didn't name the competitor, but they didn't have to. Free AI tools, primarily OpenAI's ChatGPT and Claude, are already cannibalizing price-sensitive filers who used to pay $60 to $150 for TurboTax.

Here's where the narrative flips: Intuit knows this and has chosen not to fight it. In 2024, Intuit signed data integration deals with both Anthropic and OpenAI. TurboTax is now embedded inside ChatGPT and Claude as a native tool. The company is pivoting from tax software vendor to financial data layer for AI applications. If you're filing your taxes in ChatGPT, Intuit still processes the return, still holds the relationship, and still extracts margin. They're betting the software will disappear into AI and they'll own the infrastructure underneath.

That bet might work. It might not. The market clearly doesn't trust the execution yet, and with good reason. Intuit's core business generates 70% of revenue, and that core is under structural pressure from free alternatives. The company hasn't articulated a clear path to replacing that revenue through AI integrations. They're not losing money. Their credit-card processing business (Cash App, Square payments) is still growing. But the tax software moat is eroding faster than their new bets are printing revenue.

The dip trade hinges on a single belief: that owning the financial data layer inside major AI models is worth more than selling standalone tax software. Right now, that's a thesis, not a fact. The stock has fallen 35% from its peak in September 2024. At current valuations, the market is pricing in significant share of that moat loss. Whether that's overpriced depends on whether you believe Intuit's AI deals will actually scale.

For ViewDAO readers, the signal isn't the earnings miss. It's the silence from Intuit on the DIY segment and the lack of revenue guidance tied to the AI partnerships. Until they connect those dots publicly, every rally is a sell.