ViewDAO

ViewDAO

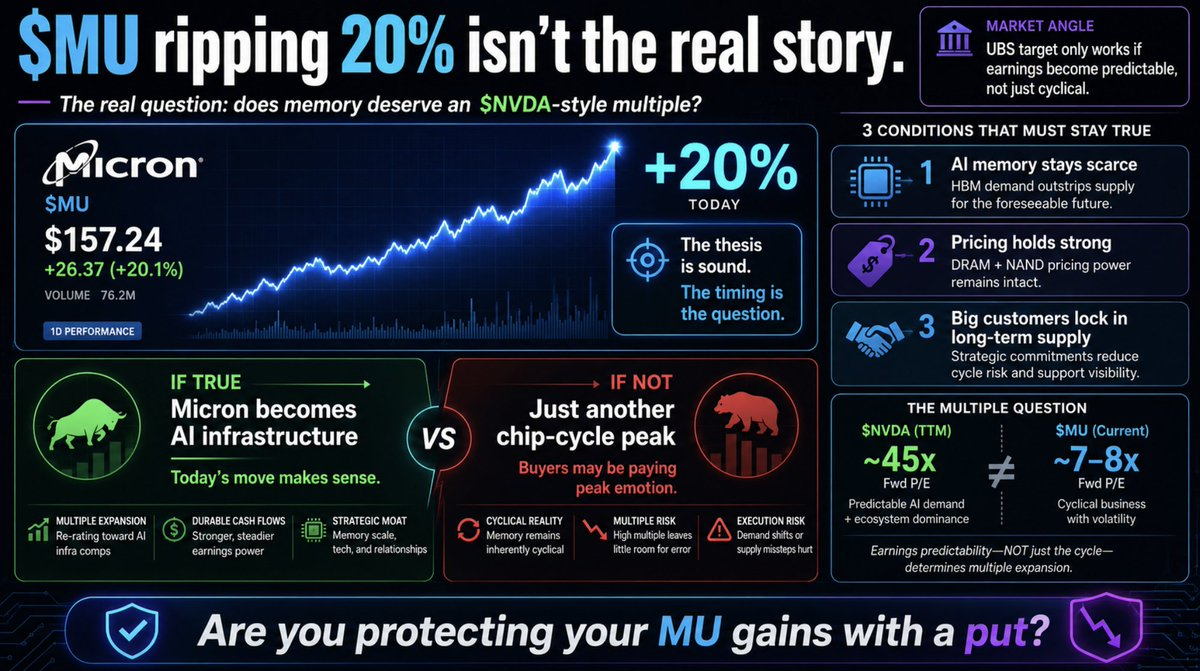

$MU ripping 20% isn't the real story.

The real story is the market testing whether memory deserves an $NVDA-style multiple. UBS moving the target to $1,625 only works if investors believe Micron's earnings are becoming predictable — not just another chip cycle peak.

That requires three things to stay true: AI memory stays scarce, pricing holds strong, and big customers keep locking in long-term supply.

Here's what makes the bull case credible: Micron's CEO said customers are only receiving 50–67% of their memory requirements right now. You don't need demand to accelerate — existing demand can't even be met. That's a supply constraint moat, not a cycle.

$MU just crossed $1T market cap. Arcuri is calling it an "AI-native infrastructure" company, trading at the same P/E as $NVDA. That's not just a price target — it's a reclassification. When institutions change how they categorize a stock, that's what drives multi-year runs, not one-day pops.

If that thesis holds, today's move makes complete sense. If it doesn't, today's buyers are paying peak emotion chasing $900 calls. Meanwhile $NVDA fades on valuation — and the money has to go somewhere.

Two very different outcomes. Same entry price.

One more thing — after a +20% day, implied volatility is elevated. Your calls made money, but the options game changes overnight.

Are you protecting your $MU gains with a put?